I currently have 3 vehicles insured with Safeco insurance.

My credit union contacted me about a discounted insurance I could get just for being a member. Had a quote done with Progressive, which would save me 500 dollars on a one year policy.

My concern is, while talking with the new agent, he mentioned that due to the age of the 88 Fiero, Progressive would not cover collision & comprehensive. He said in the event of an accident, they would value the car at 500, which is what my deductible is. Basically he said they would write the car off, take the vehicle and call it done.

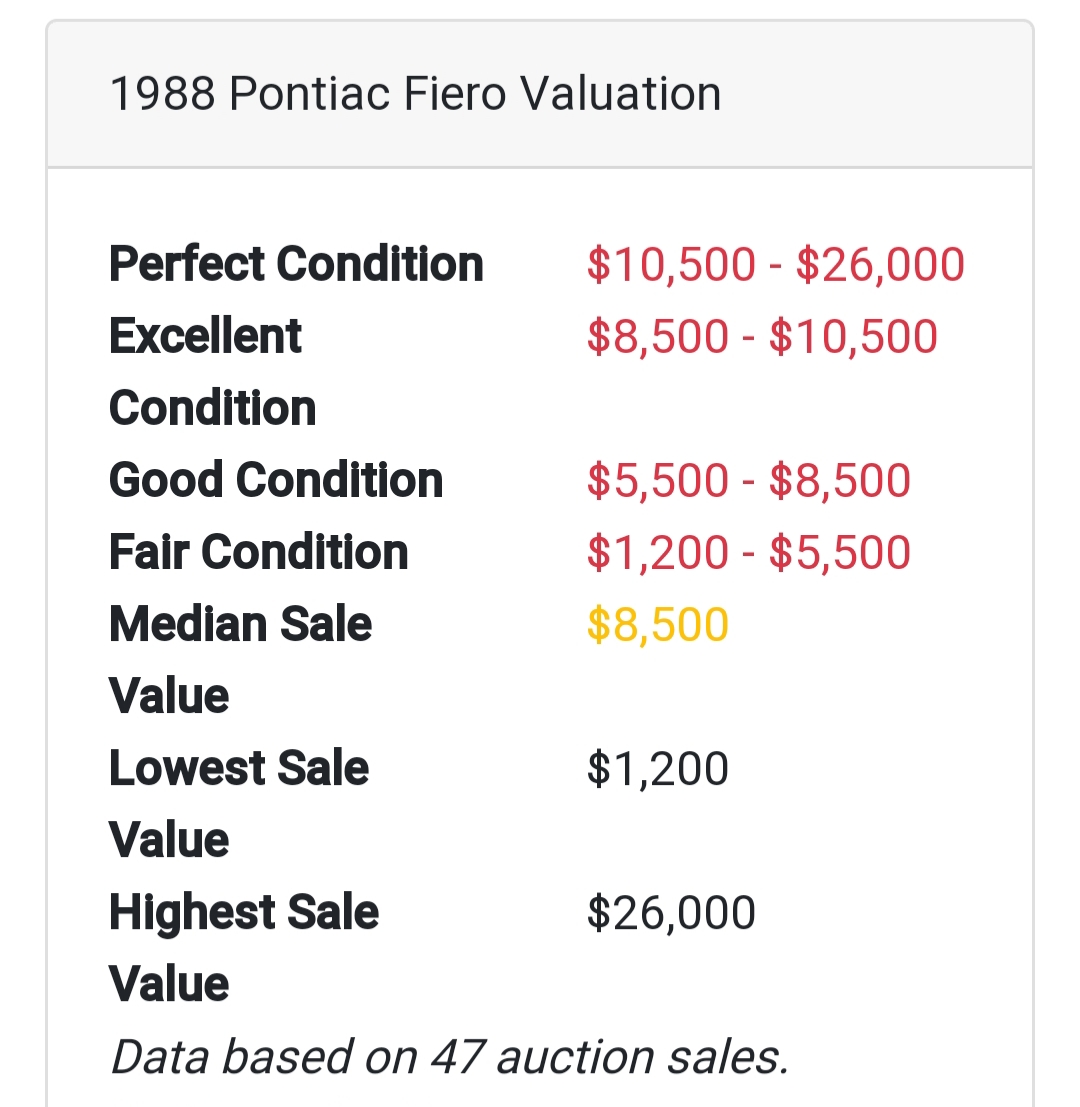

He explained they use the Kelly bluebook to rate the value. When I checked, the Fiero is not listed in Kelly blue book. Has anyone else run into this ?

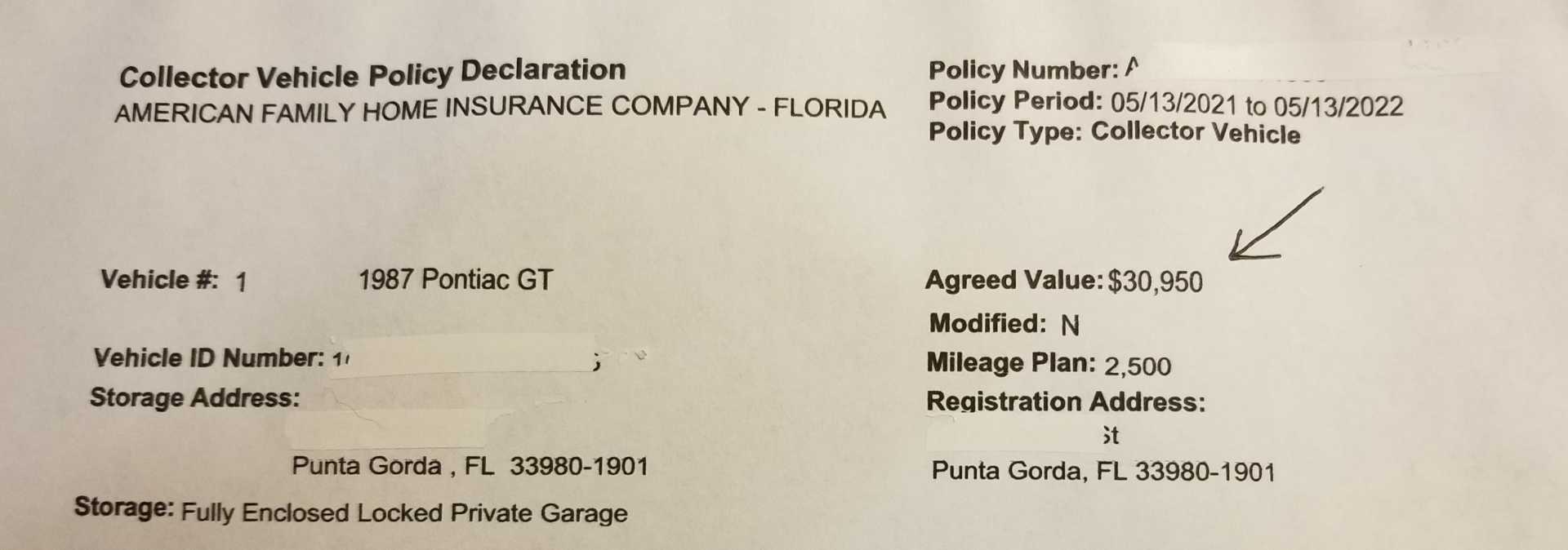

He said I could find a company that would use an agreed value, I have my 87 insured like that, those policy's have mileage restrictions, and is not for daily drivers.

I contacted my current company, asked in the event of an accident, what would they value the Fiero at. My agent couldn't answer that, they are checking with the underwriting department and will get back to me.

[This message has been edited by CoolBlue87GT (edited 03-14-2021).]

From my understanding, regular car insurance will use KBB or something similar to come up with car values when determining damages. So what you were told sounds normal to me. I have my Fiero and 54' Chevy truck with Grundy on a collector car policy with an agreed value. My insurance with full covereage from Grundy is around $500 a year for the Fiero and truck. There are no mileage restrictions on my policy but they can't be daily drivers. The occasional drive to work on a Friday or something is ok. That isn't an issue for me though as I have other vehicles to drive daily.

Progressive is awful. I swapped from them back in September because they finally broke the Camel. Took my Car, Motorcycle and Homeowners policies elsewhere. Saved me roughly 2k a year.

Most companies use kbb value.

Some companies offer actual value coverage. I do this for my bikes. What they will do is pull 3 or 4 recent sales of the same vehicle and average it out. This may be a bike only thing. Unfortunately The Fiero is a cheap car. Imho its not worth fully insuring however make sure you get uninsured motorist. Costs me roughly 250 a year. Unless.. you have a show car/historical Fiero then you can get the $$$ classic car insurance. There's limits on these as well like driving it.

Look if you have a Fiero of any real value you really need to get specified amount insurance.

Book value on these cars is nothing. Most are not worth a ton so it hurts the book value. Now if you have a very clean stock or well done modified car you need to claim the value and insure that amount of you will get nothing from regular insurance.

I have mine in under Hagerty under agreed value and it more than covers me if there is a loss. While it is collectors insurance it works for me as it is not a daily driver. It also is cheaper.

Now you can do agreed value on a daily driver but rates will go up more but if you lose the car you will get enough to cover your losses.

These cars are well beyond normal coverage unless it is just liability.

Do your home work on this to protect yourself but also not over pay.

The only "book" listed vehicles older then 25y is NADA and that and KBB values means nothing to most people at Best of times. Both "books" are total scams used by Dealer and others to rip you off. 1 is "written" and publish by a Big Used Car Co. (Cox) and KBB is from Condé Nast, both make fake values to push up prices for Used Cars from Dealers.

Any Car Insurance co can take the car only if you dumb enough to sign whatever doc w/o reading. For old cars, just 15-20y, Most will try to Total not Fix because often hard to get parts etc. If someone hits you and you make a claim on the other driver I-co, that I-co will try to pay next to nothing or Total the car. (Unless you live in a "No Fault" state that won't allow that.) Once they Total you car and if buy the car back, you will have a Salvage Title and in more and more places is hard to impossible to get a registration and tag to drive on street again. Other places will require a Special Inspection and all doc's for parts used to restore.

You find I-co don't give a F about custom paint job, big sound systems, etc. after a wreck... Just pay "book value" for the car max. Often won't even get that. But often care if find illegal "upgrades" have been done, like most Fiero Brake "upgrades," because They can and will Void any policy and leave you hanging in the wind if/when others sue you if anyone hurt/killed in a wreck.

⚠️ "Cheap" Car Insurance often leave many things out besides is often "State Minimum" policies that often haven't change payouts in Several Decades and can't pay many ER and other bills from hospital.

------------------ Dr. Ian Malcolm: Yeah, but your scientists were so preoccupied with whether or not they could, they didn't stop to think if they should. (Jurassic Park)

I have an "Agreed Value" type policy on all of my Meras with values ranging from $20k to $50k depending on the specific car. I do have to keep them garaged and have at least one other vehicle other than the Mera, but have fairly high mileage limits for each car. I have never managed to drive one anywhere the yearly limit even when driving the cars to multiple shows. Grundy is my current company but there are others.

We have Fremont Ins. I am not sure if they are only in Michigan or not. They have been very good to Us! In both cases- owned 2 Fieros at different times- I had to get the cars appraised. There is a local guy here in West Michigan that goes all over the country appraising Vettes. He also knows Fieros. He looked at the cars did some research and came up with values that were very good and the insurance company went with them. We are very happy with Fremont and have added our Home and other cars to the package. My wife works for and has in the past worked for other insurance companies. Even though she only works in accounting the first company wanted her to get the full Michigan Insurance license. Which she did and has kept it up dated for the last 18 years. She still only does accounting but still has a current Michigan Insurance License plus CSIR. She has said it is crazy not to have medical coverage in case of an accident, weather it is your fault or not. Medical costs are out of site and it doesn't take long to go though the insurance $$ So we have coverage & we have he higher limit! I would not change it. It is just plain silly not to!

[This message has been edited by solotwo (edited 03-20-2021).]

I have to say screw progressive. I have had a policy with them for over 23 years, no tickets and no claims.. They just sent me my renewal rate for the next 6 months...21% hike in premium. I called and they said their costs go up, mine goes up...when cost goes down - they lower my rates. My rates have went up 5-20 bucks a year for the last 23 years and the recent hike is just too much. I am shopping and looking close at state farm at the moment.

People, quit getting ripped off. Just get liability and sock away whatever you would have paid for your comp/collision every year into a slush fund. Within 4 years you'll have enough to replace the car even if totalled.

I have Grundy on my car $25,000 agreed value, high limit liability, no deductible, anual premium is $216.

Here's Grundys use limits:

How Can I Use My Car?

Grundy wants you to enjoy your car, not keep track of mileage like some programs with limitations. Therefore, we give you unlimited miles for pleasure driving and in collector car-oriented activities. It is even OK if occasionally you drive your collector car to work to show it off to friends. However, your collector car must not be used as a daily driver. We require you and all licensed drivers in your household to have a modern car for everyday use.

When you have your car at home, it must be kept in an enclosed, secure garage when not in use. If you are away from home on extended outings your car is fully protected if you must park it outside, for example in a hotel parking lot. Grundy coverage includes Trip Interruption that reimburses you for hotel and repair costs in the event of a breakdown, and we also reimburse you for towing and labor charges up to $250. You can count on Grundy as you cruise.

I actually sell insurance for Progressive (For real)

Call Progressive direct sales, not an agent. Depending on your value you may want an agreed value policy. Comparing rates to other folks won't do any good, there are too many variables. Also depending on your state (looking at you Florida and Michigan) each time a stupid insurance law passes prices across the board get hosed which you see on your renewals often times.

It's always a good idea to shop your insurance at least every other year though.