Please do not turn this into a political thread. 😉

Here in Europe (and especially in the Netherlands), everything has become incredibly expensive since the war in the Ukraine. Gasoline prices are up by 35% since last year, while gas and electricity prices are up by almost 300%. I used to pay around €175 per month for gas and electricity. That's is now €285 per month even though I have almost halved my gas consumption (by simply not heating my house anymore).

Grocery prices are up by 17% and the Euro has dropped to where 1 Euro is now about 1 US Dollar. Making everything else a lot more expensive as well. And it's going to get worse before it's going to get better... 😕

Please do not turn this into a political thread. 😉

Good luck with that. You know what some of these guys are like. They can't take a dump without blaming whomever for the need to do so.

Here on the west coast of Canada... food (grocery and/or restaurant) and especially gasoline prices have shot up dramatically. No one likes paying more for anything, but for me the price increases are tolerable.

Perhaps though because it's generated here with hydroelectric dams, electricity prices haven't seemed to have taken off.

For a wide variety of reasons, I feel very fortunate to be living in this part of the world.

[This message has been edited by Patrick (edited 07-15-2022).]

Sounds similar to what we have going on here. Electricity isn't that bad, yet. Cars (new and used) are getting more expensive. New cars are in short supply supposedly because of chip shortages. Fuel prices are starting to go down, but not very much. The prices of meat are likely to get very expensive in the coming year due to the price of fuel and extremely high price of fertilizer and other chemicals farmers use. Life is certainly getting expensive here, I would attribute it to a perfect storm of multiple reasons, the war, COVID, unethical companies, bad leadership, etc.

Very little of our inflation in the United States is being caused by the war in Ukraine.

Things have costed more, but I'd say on the range of about 20%.

Leading up to March of this year, just prior to Russia rolling tanks into Ukraine, the cost of gasoline was about ~$3.80 a gallon, national average. That's about $1.60 more than it was in January of 2020. So since the 2020 election, gas has doubled in the United States.

Since almost everything in the United States is either transported by truck, plane, or train within the country... the doubling of fuel costs resulted in a significant impact of everything else being sold in the U.S.

The United States, up through January of 2020 was completely energy independent. Unlike Europe, we produced the vast majority of the fuel that we used in the United States, and we only purchased foreign fuel (at that point) if it was cheaper on the international market. To make something political of course, would mean that I would be imposing opinions. So I'm not going to do that. Our "energy policy" changed in the new administration, and the following changes were made:

- Cancelled the KeyStone XL Pipeline, which would have run Canadian oil directly to a refinery which would have increased production world-wide. - Cancelled all drilling lease sales in Alaska and Gulf of Mexico - Immediately ended all drilling in Anwar, Alaska... effectively cancelling any leases that existed. - Made illegal fracking on all public lands (rendering the majority of the existing leases useless) - Doubled the amount of regulation and red-tape required to get an oil lease passed - Line5 was even cancelled, but was eventually reversed through encouragement from Trudeau.

This had a dramatic effect on the cost of everything in the United States.

All of that said, both European countries, as well as the United States, has been spending significantly above their GDP, and this has resulted in classical inflation of prices.

If we still had all of our energy policies of 2 years ago, the United States would not really be as badly affected by any of this. We would likely only suffer from the costs associated with products that come from Eastern Europe and any increased fuel costs associated with the price of goods coming internationally.

Yes I feel prices have gone up here in 2022; however to me it is not due to the war in Ukraine. Probably a small percentage of due to the war it is not the primary driver. I would say gasoline inflation is similar to what you are seeing. In June our local utility increased their price by 38%.

Most of where I see inflation is in the grocery store and in chemicals (pool chlorine).

Most of what I see driving the price increases are 1) labor costs [increased wages due to labor scarcity] 2) corporate profits 3) increased transportation costs. Example: Expensive diesel fuel and or the ~10X cost increase for containers across the Pacific.

What am I doing personally in response to increased costs? 1) I work remote instead of going into the office. saves ~$10 per day in fuel 2) Drive an old car, still driving the Honda Accord my wife bought new in 2002 with 320k on it. [why do I need a new car if I don't drive it? see above bullet] 3) Using what we already have. I stock up on items in the pantry (not a hoarder, but close). since April timeframe if we have been trying to pair down the pantry and freezer due to increased retail prices. 4) Work on my own stuff. Example from last week: A/C stopped working....thanks to youtube indented it as bad capacitor. Ran to the local distributor and $10.42 and I fixed it that day. Alternatives were a $350 service call, or even ordering the capacitor from Amazon for $25 and have to wait a few days.

Recently reported that our CPI or overall inflation is above 9%.

Yes, things have been getting more expensive. Especially gasoline, but we also are aware that it isn't near the price that Europeans pay for fuel.

Utilities are up a bit, some commodities actually have decreased because we are finally getting some things moving since Covid lockdowns, such as lumber.

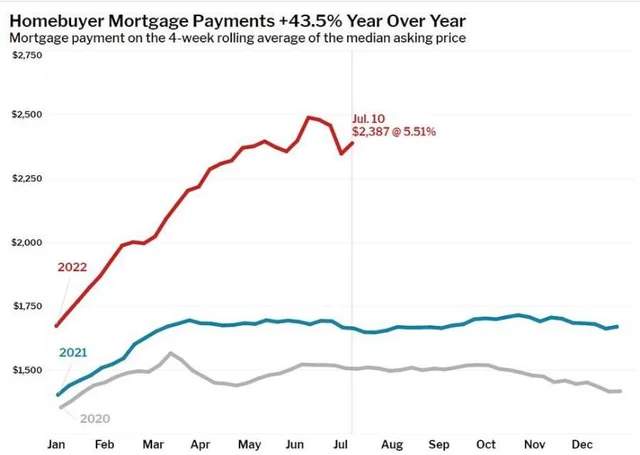

What has been utterly ridiculous, but doesn't much effect me other than property taxes, is the insane housing prices. I've never seen housing prices rise so fast and I have no idea how. It isn't like wages has kept up with these housing prices and I have absolutely no idea how a typical normal average family even affords them. It is beyond me.

Did people just suddenly inherit a load of money from dead boomer parents or something?

Anyways, brace for a worldwide recession and these prices to truly never come back down due to inflation and continued scarcity.

Yes, things are much more expensive in CONUS but for a variety of reasons, and not just the Russ/Ukraine war. Putin is certainly evil but our inflation problems began back in early 2021.

A Walmart entry level push lawnmower that just a few years ago was around $150 is now over $300. Romex 12/2 w ground is an unbelievable $2/ft price now. I've seen milk as high as $4/gallon and burger for $4/lb. Chicken and pork not much cheaper.

'officially' the price of everything is up 10%, in reality the cost of everything has about doubled. Most people are predicting a recession by the end of the year (if we aren't in one already).

Everything has gotten more expensive since Biden was elected. Although in my area gasoline prices have dropped about $0.80/ gallon (to around $4.00/gallon) recently. Basic costs have risen i.e. my barber will increase haircut from $15 to $20 starting Aug. 1. Hotel rooms have dramatically increased the even Microtel or Comfort Inn rooms run $130 plus/night. Food costs have also increased. I just roll with it and haven't been traveling as much, but with the "covid crisis" not much traveling is going on for me. I don't believe the "war" has much to do with prices, but the socialist agenda of the current party in power and their incompetence is doing the damage.

[This message has been edited by Old Lar (edited 07-15-2022).]

I think (in North America anyway) the war is (mostly) a scapegoat.

I agree with you. I would never expect the current administration to do anything less and not just the guy currently in charge, there are 40 year government veterans that have been pointing fingers for as long as they have been in office. (yeah I know the current guy is also one of those crowd.) I hope that the contributions to this smoke screen end at just sending money and are not escalated to joining the conflict. But end of the day inflation started before the war and has continued thanks to the policies of our administration.

Back to Cliff, no I do not think the war has made life in the US incredibly expensive but it has contributed.

What has been utterly ridiculous, but doesn't much effect me other than property taxes, is the insane housing prices. I've never seen housing prices rise so fast and I have no idea how. It isn't like wages has kept up with these housing prices and I have absolutely no idea how a typical normal average family even affords them. It is beyond me.

Did people just suddenly inherit a load of money from dead boomer parents or something?

I was thinking about that the other day. I'm convinced the reason why housing shot up so quickly was because of a convergence of a few things: 1 - The availability and ability of "work from home" jobs: COVID kind of brought this out... both my neighbors work from home, and even I now work from home. It's crazy how many people are working from home:

2 - Foreign Investors: I suspect in addition to what I'm going to say in #3, I think everyone potentially saw inflation coming. The only thing that really protects you against inflation, are hard assets. Gold is something that people fiddle with, and I'm not into it. But real estate is something that's tangible, it's a limited quantity, and people need it. Here in South Florida, 1 out of every 3 homes being purchased was done by a foreign investor or a corporate investor.

3 - Insanely Low Interest Rates: The insanely low interest rates we had just a few months ago are unlike anything we've ever seen in the history of our country. Not since 2006-2007 (which also caused a mad-rush to buy) did we see low interest rates. I was shocked, but I looked up prime interest rate by quarter / by year, and couldn't believe it. Under Carter, the interest rates hit 20%... but even under Reagan, they dropped to maybe 9% near the end. I'll have to try to find the link... but based on how high interest rates have historically been, the interest rate NOW is still considered a fantastic deal. It's absolutely crazy when you think about it... we were paying ~3% interest on home loans. People could afford SIGNIFICANTLY bigger and more expensive homes simply due to the fact that they were basically just paying taxes and principle.

I think when it comes down to it... with all those things combined, people just went for broke and decided to go for it, knowing that interest rates would eventually go back up, and with there being a shortage... it's like being on a cruise ship and a buffet. Everyone gets crazy because they think the ship will run out of food (which they never do).

Insanely Low Interest Rates: The insanely low interest rates we had just a few months ago are unlike anything we've ever seen in the history of our country... People could afford SIGNIFICANTLY bigger and more expensive homes simply due to the fact that they were basically just paying taxes and principle.

I think when it comes down to it... with all those things combined, people just went for broke and decided to go for it, knowing that interest rates would eventually go back up...

Yep, "broke" is a good way of putting it. All those people who overextended themselves and bought bigger/nicer houses than they could actually afford, simply because mortgage rates were (temporarily) low... are now screwed with the mortgage rates taking a large jump upwards. (Not sure about the States, but they certainly have in Canada.) Monthly mortgage payments will swell beyond reach. The piper has to be paid eventually. For a lot of people, homes will now need to be sold... for less than they were bought for.

[This message has been edited by Patrick (edited 07-15-2022).]

Yep, "broke" is a good way of putting it. All those people who overextended themselves and bought bigger/nicer houses than they could actually afford, simply because mortgage rates were (temporarily) low... are now screwed with the mortgage rates taking a large jump upwards. (Not sure about the States, but they certainly have in Canada.) Monthly mortgage payments will swell beyond reach. The piper has to be paid eventually. For a lot of people, homes will now need to be sold... for less than they were bought for.

Based on the above posting, I have to assume that variable home loans are a big deal in Canada. Initially low interest rates that can rise/fall within agreed upon limits (normally set by the lender). If so, those can be a real problem and I'm surprised people use them. Other than variable mortgages, I don't see interest rates breaking anyone. You buy a home with a set mortgage; you've agreed to (that you can afford), you make the payments for as long as the loan lasts or till you go broke. If people buy a home they can't afford, who's fault is that?

My home is paid for. Considering maybe buying another or take over the payments from one of those folks who did fall into the variable mortgage trap. I didn't set that trap but, I see no reason to not pick up the pieces when someone else's dreams fall apart.

Edited: Oh, to respond to Cliff's initial question. Yes, it is already very expensive for middle- and lower-income families. Everything we consume is affected by the price of energy (fuel). Being on a fixed income (retired), I've considered going back to work just to keep the boat afloat but, we're not taking on water (yet) and limiting our travels somewhat allows us to keep going without too much pain but, I know folks that are hurting financially, the price of fuel is really stretching their resources.

Rams

[This message has been edited by blackrams (edited 07-16-2022).]

Edited: Oh, to respond to Cliff's initial question. Yes, it is already very expensive for middle- and lower-income families. Everything we consume is affected by the price of energy (fuel). Being on a fixed income (retired), I've considered going back to work just to keep the boat afloat but, we're not taking on water (yet) and limiting our travels somewhat allows us to keep going without too much pain but, I know folks that are hurting financially, the price of fuel is really stretching their resources.

Rams

We are the same. Prices are kicking the crap out of us, and some of my little "projects" are taking a lot longer than they should just because of waiting on finances...

But we are not in debt to anybody, have a roof and food, a good town to live in with mostly friendly people, and some resemblance of health.

Yep, "broke" is a good way of putting it. All those people who overextended themselves and bought bigger/nicer houses than they could actually afford, simply because mortgage rates were (temporarily) low... are now screwed with the mortgage rates taking a large jump upwards. (Not sure about the States, but they certainly have in Canada.) Monthly mortgage payments will swell beyond reach. The piper has to be paid eventually. For a lot of people, homes will now need to be sold... for less than they were bought for.

I could go on forever on this... the dynamic is so significant, but when it comes to housing, I call this latest generation the "HGTV" generation. Because of all the shows on HGTV, Social Media, and the pressures of needing / wanting to feel like you've made it... most younger families today skipped the entire "starter home" process. They went directly for luxury homes, homes that included things like solid wood cabinets, quartz countertops, stone facades, 4+ bedrooms, etc. In doing this, many of them have over-extended their budgets. Many people do this because they need to compete with their friends on Facebook, Instagram, etc... where everyone has a luxury home with luxury appliances, etc.

I don't know about the comment though about their mortgage rates increasing. Most people today purchase homes at a fixed interest rate. 30-Year "Fixed." It's not like it was in 2007 when you had a lot of people with adjustable rate mortgages.

I have two mortgages, one on my rental property, and one on the home I live in today. Both of them are about 3% interest rate. That rate will never change, and it'll stay the same for the life of the mortgage. Most people have mortgages like this too, so it's probably more a feeling of "they got in while the getting was good." But moving forward, a $400k home that would have normally cost you $2,200 a month (with insurance + taxes), is now going to cost people $2,750 with today's rates if you were to buy that $400k home today at 6% instead of 3%.

If interest rates continue to climb and go back up to around what they were in the 80s and 90s... then I suspect people will have to start buying smaller tract homes like people had in the 50s and 70s. Unless supplies / materials go WAY down in price, which could lead to people being able to buy larger homes for a comparable price.

One thing is for sure, rents are going to keep going up... and homes in desirable areas are only going to increase in value.

If interest rates continue to climb and go back up to around what they were in the 80s and 90s... then I suspect people will have to start buying smaller tract homes like people had in the 50s and 70s. Unless supplies / materials go WAY down in price, which could lead to people being able to buy larger homes for a comparable price.

Lumber has dropped in cost compared to what it was a year or 2 ago. Anything metal tho is still pretty high.

I know all about 'little boxes' but not because of interest rates or other costs.

Hahahah! I will say this though MJ... homes in Florida are not made of TickyTacky... they're made out of solid concrete, reinforced with rebar!!! (Tim Allen grunts).

I totally knew where this was going. I'm 3/4ths of the way through, and convinced that the people will end up in little boxes, buried in the ground, made out of ticky-tacky.

I will say though, before I finish the song... many of these people living in the tiny boxes, also invent and design rockets that will take us to Mars. While their homes in Boca Chico are made out of Ticky Tacky, the homes on Mars most certainly will not. They'll be made out of Clicky-Clacky.

EDIT: On the lumber, I think this will eventually lead to a lower cost of home ownership, but with inflation being what it is... all the other things will continue to go up in price. I can't wrap my head around it... but 50-60 years ago, homes were made with more intricate details. You had more distinctive styles... Craftsman, Arts & Crafts, Queen Anne, Queen Victorian, Tudors, Shirtwaist... and that's just the North East and Mid-West... you look at New Orleans architecture, or South Florida architecture (Spanish or Art Deco), or South Western, or even North Western architecture... and they're all extremely distinctive.

I won't say homes are built better, because they are not. They're more modern in terms of the technology and their efficiency, but they're also more mass produced and everything is quick and cheap. But remember that a 2x4 was $1.80 just three years ago. Now it's... what, $5.70 down from $8 bucks at one point? People were building homes with mahogany and oak beams because it was cheaper than pine and poplar studs. Which is absolutely crazy in my mind.

Anyway... I can't put two and two together on where this goes... I suspect they'll build more "ticky tacky" boxes all throughout the country, and it will lead to further destruction of cultural identity and style of each of the individual states as people seek cheaper homes. I think we'll see more starter homes... but possibly, we see more older homes getting renovated.

And this brings me to my bonus rambling point. There are so many small towns in this country that have amazing, absolutely amazing old homes. I don't know about now... but 3-4 years ago, you could buy a MANSION in the town of Beaumont. I mean, literally a 5,000+ square foot home with massive entry foyer with dual staircases going up the center of the room with big chandelier and balcony... which have two-story libraries with fire places and the sliding book-shelf ladder. Homes like these were going for $70-80k... all made in the late 1800s or early 1900s in places like Beaumont, TX... or Brookfield, Missouri, or places like that. Hopefully with people being able to work remotely, they move to these smaller towns and renovate these homes. I'm sure it'll be met with mixed emotions, "city folk" moving in and bringing their liberal ways... but at least the architecture will be saved.

[This message has been edited by 82-T/A [At Work] (edited 07-16-2022).]

Well, you can just keep that left-coast wack-job, pronoun-using multi-cultural-leftist-whatever hell hole.

I wish more people felt the way you do. Seriously. There'd then be far fewer people clamoring to live in this beautiful place. It's starting to get a little crowded here on the west coast!

Based on the above posting, I have to assume that variable home loans are a big deal in Canada. Initially low interest rates that can rise/fall within agreed upon limits (normally set by the lender). If so, those can be a real problem and I'm surprised people use them.

quote

Originally posted by 82-T/A [At Work]:

I don't know about the comment though about their mortgage rates increasing. Most people today purchase homes at a fixed interest rate. 30-Year "Fixed." It's not like it was in 2007 when you had a lot of people with adjustable rate mortgages.

The housing situation in Greater Vancouver area is nuts. See my previous post. A city lot with a "knock-down" on it here goes for $1.5M... and I'm not referring to some exclusive expensive neighborhood either. So people are forced to pay more than they can actually afford if they want a house anywhere in this region.

It's no mystery then why variable rate mortgages were favored by many home purchasers. They had no choice (if they were insistent on buying a house). The rates were simply lower than they were for fixed rate mortgages. These people couldn't afford the larger monthly mortgage payments that would've been set by utilizing the higher fixed interest rate, so they gambled on the lower variable interest rate as they felt they could "afford" those smaller monthly payments. Well, now that the prime rate has shot up... those variable rate monthly payments are beyond reach for many people who had bought a place during the period of low interest/mortgage rates.

[This message has been edited by Patrick (edited 07-16-2022).]

The housing situation in Greater Vancouver area is nuts. See my previous post. A city lot with a "knock-down" on it here goes for $1.5M... and I'm not referring to some exclusive expensive neighborhood either. So people are forced to pay more than they can actually afford if they want a house anywhere in this region.

It's no mystery then why variable rate mortgages were favored by many home purchasers. They had no choice (if they were insistent on buying a house). The rates were simply lower than they were for fixed rate mortgages. These people couldn't afford the larger monthly mortgage payments that would've been set by utilizing the higher fixed interest rate, so they gambled on the lower variable interest rate as they felt they could "afford" those smaller monthly payments. Well, now that the prime rate has shot up... those variable rate monthly payments are beyond reach for many people who had bought a place during the period of low rates.

If what you're saying is what I think is going to happen, then this will be really, really bad for Canada's economy... or at least the housing market. In the U.S., we were "bitten" by the housing collapse in 2007, so they generally don't offer variable rate interest rates on homes unless there's a very specific reason why you need one.

In 2007, a ton of people defaulted because of those variable rate mortgages. Some of them even had something called a "balloon payment," which I assume was some agreed-upon payment that would take place after a certain amount of time. I just really consider myself so lucky that I got the interest rates I did, and when I did. I balked at times that I didn't try to go even lower, like 2.5% or something like that. But man do I feel lucky now.

That really sucks though... I know people don't have anyone but themselves to blame, but I really do blame social media and HGTV. Everyone wants to live in a super trendy area, and everyone wants to have ultra-luxury. What a time we live in.

Originally posted by 82-T/A [At Work]: If what you're saying is what I think is going to happen, then this will be really, really bad for Canada's economy... or at least the housing market. In the U.S., we were "bitten" by the housing collapse in 2007, so they generally don't offer variable rate interest rates on homes unless there's a very specific reason why you need one.

In 2007, a ton of people defaulted because of those variable rate mortgages. Some of them even had something called a "balloon payment," which I assume was some agreed-upon payment that would take place after a certain amount of time. I just really consider myself so lucky that I got the interest rates I did, and when I did. I balked at times that I didn't try to go even lower, like 2.5% or something like that. But man do I feel lucky now.

That really sucks though... I know people don't have anyone but themselves to blame, but I really do blame social media and HGTV. Everyone wants to live in a super trendy area, and everyone wants to have ultra-luxury. What a time we live in.

Not only did they have variable rate mortgages, balloon mortgages (really designed for property flippers), but these interest only loans. I've read people being stuck on these for a good solid 10-years before they could refinance to a loan that paid down the principle.

Not only did they have variable rate mortgages, balloon mortgages (really designed for property flippers), but these interest only loans. I've read people being stuck on these for a good solid 10-years before they could refinance to a loan that paid down the principle.

Holy **** ! I forgot about the "interest only" loans. Can you imagine living in a home for 10 years, and literally not have even a single cent of principle paid into it? You're basically renting... because then at that point, you now have to not only renegotiate for a new mortgage, but you'd have to also qualify for one too. Ugh.

If what you're saying is what I think is going to happen, then this will be really, really bad for Canada's economy... or at least the housing market.

Keep in mind that Vancouver (and Toronto) will be the worse case scenarios in regards to a housing market "correction". It's not nearly as bad in most other locations across the country.

quote

Originally posted by 82-T/A [At Work]:

In the U.S., we were "bitten" by the housing collapse in 2007, so they generally don't offer variable rate interest rates on homes unless there's a very specific reason why you need one.

There were supposedly safeguards put into place to prevent a re-occurrence here of what you're referring to, but the writing was on the wall at least a year ago that things could/would go south. There were some further steps taken to make it more difficult to qualify for a mortgage, but it was too little too late. The Bank of Canada began raising the prime rate a couple of months ago to slow down inflation, and then again levied a big increase just a few days ago (as I linked to Here).

I was house hunting prior to the pandemic, and then paused my search during the worst of COVID. I started looking again a few months ago, but the already crazy prices were literally increasing by the day. Most, if not all houses were being sold for above asking price (by hundreds of thousands of dollars, I'm not kidding*) as people were trying to take "advantage" of the low mortgage rates. Now these people are in trouble, houses will need to be sold, prices will plummet... and I'm back in the hunt. I'm so glad I didn't allow myself to be caught up in the house-buying frenzy of this past spring.

*Two months ago my neighbors put their "knock-down" of a house up for sale. It's assessed value was $1.4M, they listed it at $1.6M and it sold eight days later for $1.9M. The housing market here has been totally nuts. Hopefully it will soon get back to some semblance of "normal".

[This message has been edited by Patrick (edited 07-16-2022).]

From my perspective, yes... things have gotten more expensive. Gas is stupidly high (for the US) - up ~60% - and so are other things. Most of our groceries are ~20-30% higher, just guessing. Our electricity hasn't gone up very much, but there is a "rate case" in the works that will allow an increase of ~10%. This isn't really a show stopper for us, since we mostly stay home (we're both retired) and don't buy a lot of stuff other than food, and "junk" that we want from Amazon and such. We might eat out once a week. That got expensive when COVID happened, and has continued that way.

[This message has been edited by Raydar (edited 07-16-2022).]

The housing situation in Greater Vancouver area is nuts. ..............

It's nuts everywhere dude.

We had to "pull strings" and get Kim's health workers involved to get into this place. Regular waiting list to get in is 4-5 years. IF (and I mean if) you can get approved. THAT took a sheet-ton of interviews, phone calls and assurances.

[This message has been edited by MidEngineManiac (edited 07-17-2022).]

The housing situation in Greater Vancouver area is nuts. See my previous post. A city lot with a "knock-down" on it here goes for $1.5M... and I'm not referring to some exclusive expensive neighborhood either. So people are forced to pay more than they can actually afford if they want a house anywhere in this region.

It's no mystery then why variable rate mortgages were favored by many home purchasers. They had no choice (if they were insistent on buying a house). The rates were simply lower than they were for fixed rate mortgages. These people couldn't afford the larger monthly mortgage payments that would've been set by utilizing the higher fixed interest rate, so they gambled on the lower variable interest rate as they felt they could "afford" those smaller monthly payments. Well, now that the prime rate has shot up... those variable rate monthly payments are beyond reach for many people who had bought a place during the period of low interest/mortgage rates.

It's unfortunate that people just can't settle for what they can afford. For some reason, Forrest Gump comes to mind. We all want better for our families but, it's pretty silly to buy something you're doomed to lose when those payments go up. If, one intends to flip that home prior to the time the mortgage goes up, that's one thing but, to hope things don't go south and one's income will increase is simply wagering on the future. Too many found out betting all the eggs in that basket didn't work out.

------------------ Rams

Isn't it strange that after a bombing, everyone blames the bomber, his upbringing, his environment, his culture, his mental state but … after a shooting, the problem is the gun.........

If one intends to flip that home prior to the time the mortgage goes up, that's one thing...

I certainly don't feel sorry for the "flippers" when they get burned. There was quite a scam going on here that supposedly has been curtailed, but it was the real estate agents themselves who were flipping homes for huge profits. Scumbags.

I certainly don't feel sorry for the "flippers" when they get burned. There was quite a scam going on here that supposedly has been curtailed, but it was the real estate agents themselves who were flipping homes for huge profits. Scumbags.

My one regret is that when I got out of the military, I didn't go into real estate. I know several folks who did and they are all much better off than I am financially, have more time off and don't sweat the details that I do. My problem is, I have a hard time lying with a straight face. Edited: Actually, they don't lie, they simply don't tell the whole truth.

Rams

[This message has been edited by blackrams (edited 07-17-2022).]

My one regret is that when I got out of the military, I didn't go into real estate. I know several folks who did and they are all much better off than I am financially, have more time off and don't sweat the details that I do. My problem is, I have a hard time lying with a straight face. Edited: Actually, they don't lie, they simply don't tell the whole truth.

Rams

If you look at the wealthiest Americans, with the exception of those who were part of creating something (working at a tech company, or some big invention for the time)... the rest of them almost always made their money via real-estate.

...the rest of them almost always made their money via real-estate.

I would've thought it was through importation/distribution of illegal drugs and/or booze (during prohibition). Or maybe that was just seed money to use to then buy up all the real estate. I'm being serious!